Reverse For Purchase

Use a reverse mortgage to purchase your next home!

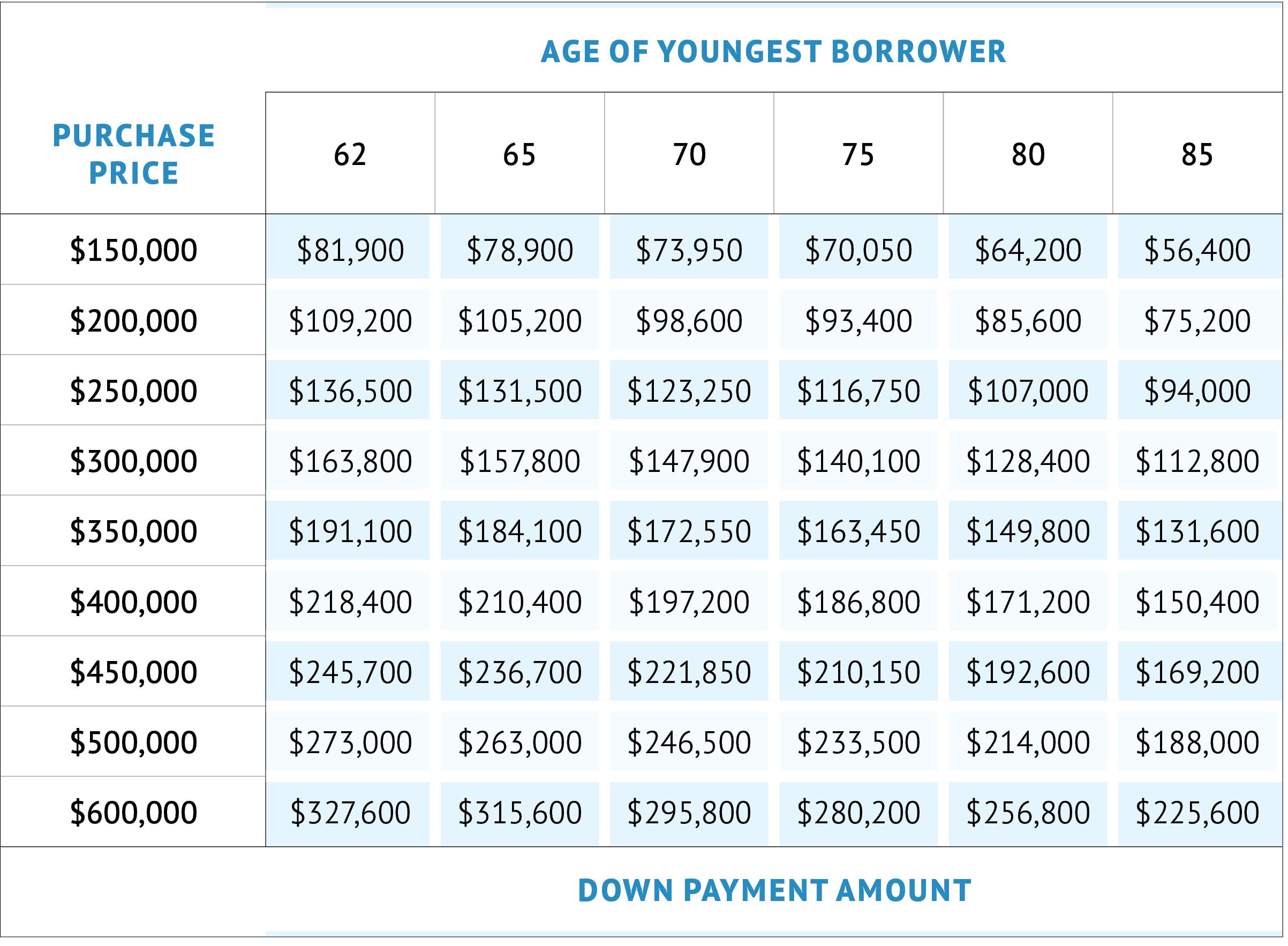

Down Payment: The funds from your new reverse mortgage will go toward a percentage of the home’s purchase price, and your down payment will pay for the rest. You can use cash from the sale of your previous home for the down payment. Click here to see what your down payment could be.

No Monthly Mortgage Payments: No monthly mortgage payments are required on the new home, but you can still make payments, just like a traditional mortgage.* You only need to follow the loan’s terms and pay your other payment obligations such as property taxes, homeowners insurance and maintenance.

Move to a Home Better Suited for You: You can live closer to friends and family, move to a more fulfilling community, or purchase a home more tailored to your needs. Retirement is your time!

Reverse for Purchase

A HECM for Purchase can help you purchase a home with a reverse mortgage. By using the proceeds from the sale of your home (or other assets) with your new reverse mortgage proceeds, you can purchase a home in one single transaction!

This unique reverse mortgage carries the same great benefit of having no monthly mortgage payment!* You only need to follow the loan’s terms and pay your other payment obligations such as property taxes, homeowners insurance and maintenance.

Reverse For Purchase Features

- Purchase a home with your reverse mortgage proceeds

- Down payment depends on home price and age of youngest borrower

- Home must be your primary residence

- Move to a retirement community, closer to family and friends, or a home better suited for your needs

- Single-family homes, townhomes, and approved condos

Reverse For Purchase FAQ’s

Find answers to some of the most common questions about reverse for purchase inquiries.

Can I still make monthly payments?

Absolutely! Many reverse mortgage borrowers choose to continue making payments to lower their loan balance, just like a traditional mortgage. A reverse mortgage allows homeowners the option to make monthly payments to avoid any stress if you can’t pay your mortgage payment. Just like a traditional mortgage, you still pay separate property taxes and insurance.

How much will I need for a down payment?

Minimum down payment amounts vary depending on the type of loan. For instance, FHA loans have a low down payment requirement of only 3.5%. With a conventional loan, borrowers will need to put down at least 5% or at least 20% to avoid paying private mortgage insurance. VA or USDA loans have no down payment options.

Are there restrictions on how I can get money for my down payment?

Your down payment must be your own money or money obtained from the sale of your current home. You can draw money from your savings, and monetary gifts from a family member are permitted. However, the money cannot be borrowed from a family member, a bank, or any other funding source that you will need to repay. That also includes borrowing against an asset such as a CD or life insurance policy.

Can I refinance a Reverse for Purchase?

Absolutely. If your home appreciates in value, your equity grows, and you may become eligible to refinance and access some of that equity! The equity proceeds from your initial reverse mortgage are used to finance the home, but refinancing your HECM allows you to access tax-free1 cash to use however you’d like!